AI Needs a Better Founder Narrative.

Mary Meeker gave us the macro map. Here is where the moats are actually forming a year later.

Last year, around this time, Mary Meeker released a 300-pages AI report and everyone in my circle was talking about it. That reaction was not just about her name. It was about what her work has represented in earlier technology cycles - a serious attempt to turn a noisy market into a readable map. so it was obvious that the market paid attention straight away. I also noted then that she does not publish these heavyweight trend decks every year, and when she returns with one, people expect more than commentary. They expect a frame for what is actually happening.

I did a youtube video on it then which covered the findings in detail.

Looking back at it, that timing was quite interesting. By mid-2025, AI was no longer just a product story or a lab story. It had become an infrastructure story, a capital allocation story, a work story, and increasingly a geopolitical story.

The market did not need another stream of launches. It needed a synthesis. and Meeker’s report gave that synthesis.

It argued that adoption, usage, capex, model progress, and competition were all accelerating at unusual speed, and it backed that claim with a chart-led case that AI was becoming a compounding system rather than a passing software theme.

What it did not fully answer however, at least from my impression of it, was the founder question.

It showed scale. It showed speed. It showed momentum. But it did not really tell founders where value was settling, what was already becoming a commodity, or how to think clearly in a market where every week now produces fresh claims about breakthroughs, agents, competition, and disruption.

A year later now, the broad thesis still looks strong. Adoption has kept rising. Enterprise usage has broadened. AI budgets remain elevated. The newer data suggests Meeker was broadly right on the direction of travel and, in some areas, conservative on the pace. But that is exactly why this essay is worth writing now. The useful question is no longer whether her report was “right” in the abstract.

The better question is whether it still helps founders make sense of what is happening now, and where a founder needs a sharper lens than a macro deck can provide.

In this deep dive or long essay I am taking Meeker’s report as a starting point, and not end point. and looking at

why the report landed the way it did, what it actually captured, what it left open, whether the thesis has held up after a year, where the market has moved faster than expected, where it is still behind, and what founders should watch next.

Note - for those looking for Anthropic playbook part 3 - with so much happening, I thought i’d push it a bit further down the line, and closer to IPO time and have written a short take on Fable on AIUnfiltered here.

Table of Contents

Why Meeker’s report landed the way it did

What the report actually captured

What it left open for founders

Has the thesis held up after a year?

Where the market moved faster than expected

Where the market is still behind

What founders should take from it now

What to watch by next year

1. Why Meeker’s report landed the way it did

Mary Meeker’s report arrived with unusual weight because it felt like the return of a format the technology world still trusts:

the big trend deck that tries to explain the cycle, not just the week.

Her earlier Internet Trends reports mattered because they gave people a language for understanding transitions that were already underway but not yet widely organized in public thinking. One of the other and main reason the 2025 AI report landed in a similar way was because

AI had reached the point where the market had too much INFORMATION and not enough STRUCTURE.

That is what made the report highly anticipated. By the time it came out, the public conversation around AI had become fragmented. One part of the market was fixated on model releases. Another was focused on GPU supply and cloud capex. Another was watching regulation. Another was already talking about agents and workflow automation. These were all parts of the same system, but they were rarely described together. Meeker’s report tried to put them on one page, or rather 300-plus pages.

Her own framing makes that clear. In the report’s context section, she writes that a collection of datapoints became “this beast,” and that the charts kept needing to be updated because the moving pieces were all affecting one another. That is a useful line to hold onto because it captures the real shape of the market.

AI is not moving as one clean curve. It is moving as a set of connected curves: users, compute, capital, products, competition, and geopolitics.

That why I actually care about it and so does the market imo. The market did not need another bullish report. It wanted orientation. It wanted to know whether AI should be read as a normal software wave, an infrastructure reset, a bubble, a productivity revolution, or something larger.

Meeker’s answer was that it looked larger. and I agree.

ref: page 3, “Context.”

ref: pages 8–9, “Overview.”

( I can’t add too many images because of sizing issue, so am adding the reference here in each section if you want to look deeper, the current maps I have created however should be enough to follow through otherwise. )

2. What the report actually captured

One of the strengths of the report is that it was broader than a lot of the commentary around it. It was not only about frontier models or consumer adoption. The outline itself shows the full range, for example change happening faster than ever, AI user and usage growth, capex growth, model compute costs, falling inference costs, rising competition, China’s rise, the physical world, global diffusion, and work evolution.

That matters because it means the report was not simply arguing that ChatGPT got big quickly. It was making a larger case that AI had become a compounding system built on internet distribution, accumulated data, model scaling, developer ecosystems, cloud infrastructure, and aggressive capital deployment. The best summary of that appears in the “Charts Paint Thousands of Words” pages, where the report compresses its core argument into a small number of flagship visuals.

A few charts carry most of the narrative load. The leading US-based LLM user chart on page 55 is central because it captures the speed of user growth. The comparison of global adoption outside North America on page 56 matters because it shows that AI did not diffuse the way earlier internet platforms did; it spread globally almost from the start. The Big Six US technology company capex chart on page 97 matters because it makes clear that this is not only an app story but also a capital buildout story. And the inference cost chart on page 138 matters because it shows why usage can keep rising even while training and infrastructure remain expensive.

The report also deserves credit for reaching beyond software. Its physical-world section, while short, points toward automation and autonomy moving into real operating environments, with the San Francisco autonomous taxi market share chart on page 302 acting as a visible proxy for that shift. Its work section does something similar, especially with the AI versus non-AI job postings chart on page 332, which helps show that AI was already changing labour demand, not just future speculation.

If the question is what Meeker captured well, the answer is this:

she captured that AI had become a multi-layer market all at once. Not just a model market. Not just a startup market. A distribution, infrastructure, labour, and geopolitical market too.

ref: page 4 or page 10, “Outline.”

pages 5–7, “Charts Paint Thousands of Words.”

page 55, leading LLM weekly active users.

page 56, global usage outside North America.page 97, Big Six capex.

page 138, inference cost decline.

page 302, autonomous taxi share.

page 332, AI vs non-AI IT jobs.

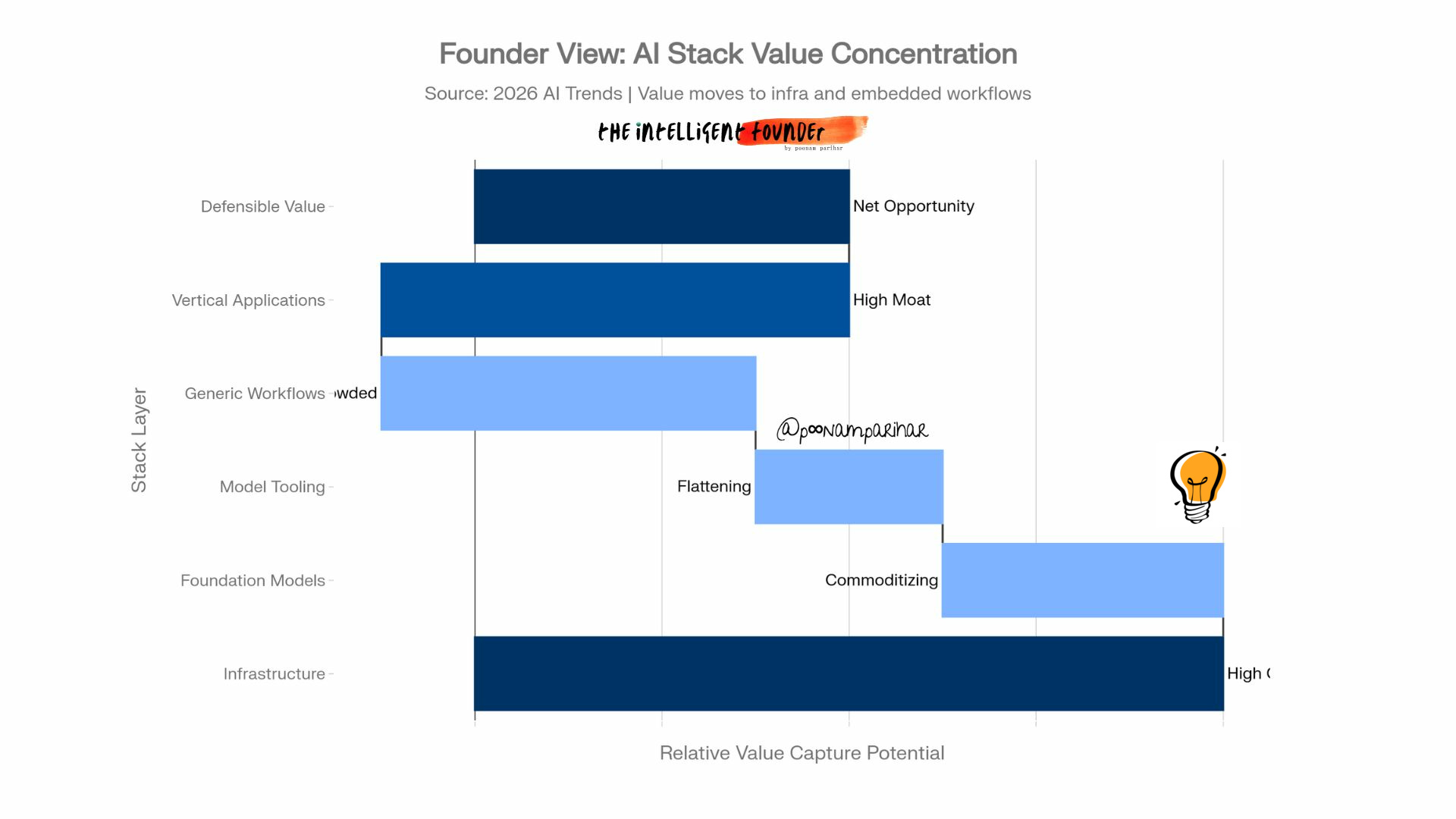

3. What it left open for founders

This is where the founder angle starts to matter. Meeker’s report is strong on scale and speed, but lighter on position.

It shows what is growing, but not always where durable company value is likely to settle.

and I am not criticizing it but rather creating a boundary. It is a macro deck. It is trying to explain the cycle. But founders still need a second layer of interpretation.

The first missing piece is commoditization.

A chart can show that adoption is rising, but it cannot by itself tell a founder whether that adoption benefits new entrants, incumbents, infrastructure providers, or workflow owners. In a market like this, growth does not automatically mean opportunity for everyone. Often it means category crowding.

The easier it becomes to ship AI features, the harder it becomes to claim that AI features alone are the business.

The second missing piece is stack position.

Public AI discussion often blurs together foundation models, tools, APIs, copilots, agents, vertical applications, and embedded operational systems. Founders cannot afford to blur them. They need to know where they sit in the stack and how value may move between layers. Some parts of the stack are scaling fast but becoming interchangeable. Others are harder to build, harder to sell, and slower to scale, but potentially more defensible.

The third missing piece is operational reality.

Enterprise adoption numbers are useful, but they do not tell a founder how hard it is to integrate AI into an existing workflow, win trust, prove ROI, manage governance, or avoid buying a dependency that later gets flattened by the platform layer.

Founders need to read AI not just as a capability wave but as a systems integration problem.

That is why a founder reading of the report is useful. The macro map says AI is real, large, fast, and capital intensive. The founder version adds a sharper question:

where in this market can a company still build durable advantage, and where is the apparent opportunity already collapsing into infrastructure, platform leverage, or commodity software?

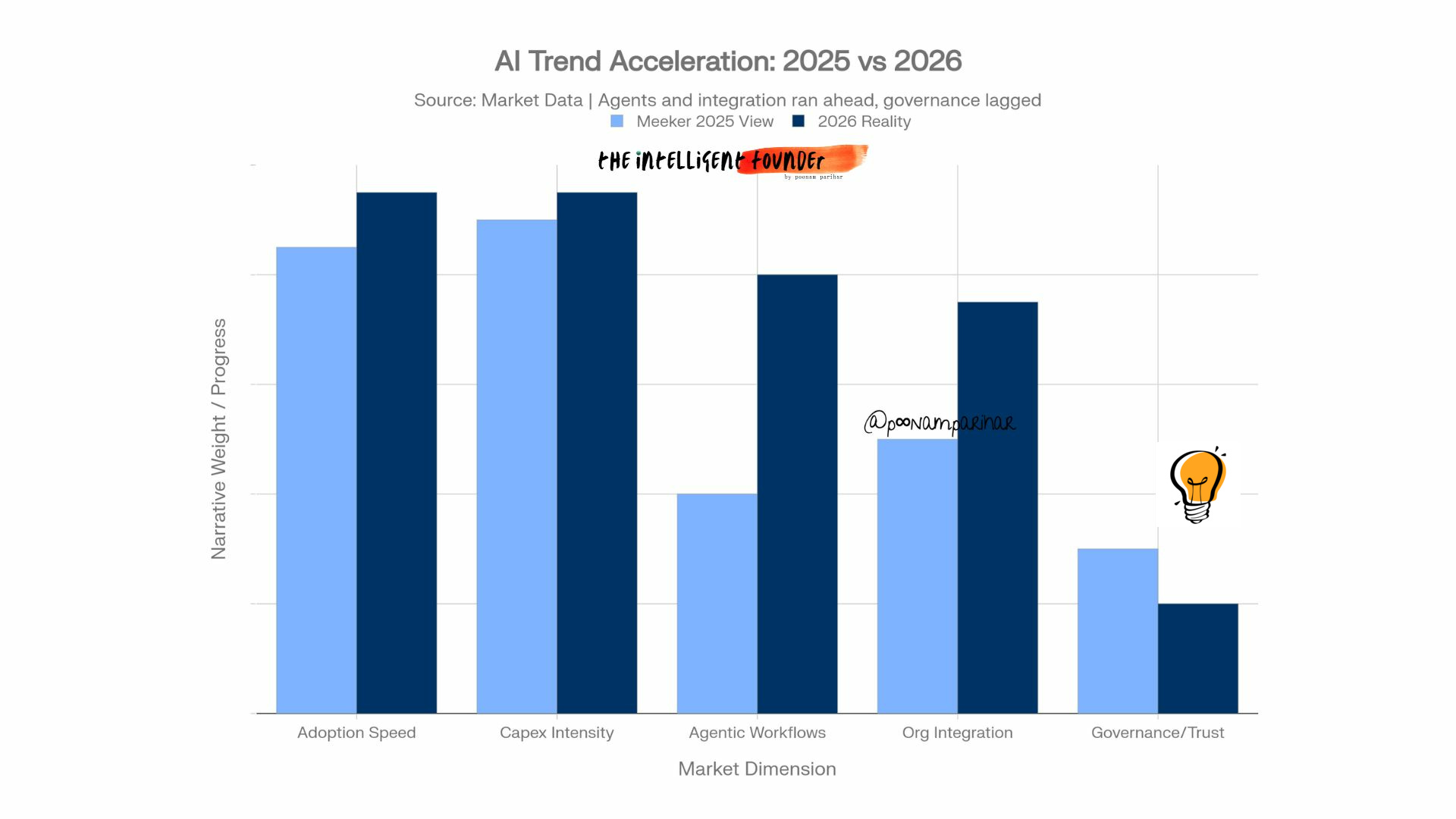

4. Has the thesis held up after a year?

Broadly, yes. specially the central Meeker thesis.

The market has continued to validate the core claims around speed, adoption, spending, and integration. Stanford’s 2026 AI Index shows that generative AI reached around 53% global population adoption within three years, and private AI investment in the United States reached about 286 billion dollars in 2025. Those figures do not suggest a narrative reversal. They also suggest the opposite that the system Meeker described kept advancing.

Enterprise data points in the same direction.

NVIDIA’s 2026 State of AI materials indicate that around 64% of organizations are actively using AI in operations and that 86% expect AI budgets to rise in 2026. That matters because it shows AI moving further from experimentation into embedded operational use. In other words, the market did not just keep talking about AI. It kept buying it, deploying it, and budgeting for it.

On capability, the broader trend has also held. Stanford reports continued gains in benchmark performance, including frontier systems matching or exceeding human baselines on difficult tasks and coding benchmarks improving dramatically over a short period. This has reinforced one of Meeker’s core arguments

that model progress and usage growth are feeding each other rather than exhausting each other.

So if the question is whether the report held ground, the answer is yes. But the more useful answer is that it held ground because the forces behind it were structural. AI was not riding only on hype. It was riding on real infrastructure buildout, falling inference costs, expanding deployment, and a market-wide effort to reorganize products and workflows around machine intelligence.

5. Where the market moved faster than expected

If the broad thesis held, some parts of the market moved even faster than many people expected.

One of the clearest examples is the shift from chatbot framing to agentic framing.

In 2025, a lot of public discussion was still anchored in assistants, copilots, and content generation.

By 2026, much of the conversation had moved toward systems that can call tools, execute sequences of tasks, and sit closer to workflow execution rather than simple interaction.

That matters for founders because it changes which product categories feel early and which already feel crowded. It is one thing to build on top of a chat interface. It is another to build around task execution, orchestration, and integration into real operational environments. The latter is harder. It is also where a lot of fresh value may move.