AI, Safety and GDP: The Blind Spot in Today’s Macro Story

How AI’s macro story misses what happens on the factory floor!

In 2025, workplace regulators started to see a new kind of incident report.

The pattern was familiar - an AI‑driven system pushed for more speed or throughput, and safety somehow got slipped.

In some cases, the system was meant to optimize output. In others, it was there to monitor the floor, flag risks, or tighten scheduling. But when sensors misread conditions, or the system failed to notice that a process had changed, the result was the same: near‑misses, unsafe decisions, and sometimes real injuries.

On paper, these were “AI productivity tools.”

On the ground, they were software systems making confident decisions with messy data on top of aging equipment and overstretched teams. That matters for more than workplace safety. It matters for the economy too. Because once AI starts showing up in productivity forecasts, labour models, and growth expectations, these “local” failures stop being local. They become part of the real story of how AI affects wages, output, and risk.

This piece looks at how AI shows up in real workplaces and in the big‑picture numbers economists use to talk about growth and GDP.

We are trying to figure out what gets missed when we talk about “AI adoption” but ignore the state of the sensors, infrastructure, and safety practices underneath. This one is aimed at anyone building, buying, or regulating AI systems in the real economy, especially founders working on AI for industry and infrastructure.

What’s inside

How AI ended up on the economic dashboard

What today’s AI stats and indices actually measure

The blind spot: messy data, old infrastructure, and safety incidents

Why that blind spot changes the AI‑and‑GDP story

A small, testable claim about AI, sensing, and real productivity

1. How AI crept into the economic dashboard

Over the last couple of years, AI has moved into parts of the conversation where it simply was not before. Economists, investors, and policymakers now treat it as something that can change the path of the wider economy, not just the fortunes of a few tech firms.

That shift is visible in several places. Researchers have built an AI uncertainty index by scanning news coverage and tracking how AI‑related uncertainty feeds into markets and labour conditions. Stanford’s 2026 AI Index includes a full economy chapter on investment, productivity, and labour exposure. The IMF now describes AI as a macro‑critical transition, something with implications for growth, inequality, and financial stability.

We can confidently say that AI is no longer just a technology story now. It is now part of the macro story.

It sits alongside interest rates, energy prices, and global demand in the way people explain what might drive the next few years.

2. What the new AI numbers actually measure

To make AI visible at that level, different groups track different signals.

Some track spending:

how much money is flowing into data centres, chips, models, and related infrastructure, and

how that compares with earlier technology booms as a share of GDP.

Some track productivity:

whether AI tools help workers complete defined tasks faster or better. In customer support, coding, and similar settings, some studies now report gains in the rough range of 15–25%.

Some track labour effects:

who is helped, who is squeezed, and how firms reorganize work.

Early evidence suggests some junior roles are hit sooner, while more senior roles are more protected for now.

And some track uncertainty itself.

The AI uncertainty work suggests that spikes in AI‑related uncertainty are linked to weaker equity prices, lower wages, and fewer hours worked, even when headline employment does not move much.

From a distance, this is all sensible. If AI is a large shift, then spending, productivity, labour, and risk are exactly the right places to look.

But this is also where the blind spot starts.

3. The blind spot: sensors, rust, and real‑world safety

Most of these measures treat AI as if it were one clean category.

A firm either “uses AI” or it does not.

A sector is either “AI‑exposed” or not.

That works reasonably well if the system lives mostly in software. It works far less well when the system is wrapped around physical operations.

In a factory, a rail network, a substation, or a water system, an AI system is not just a model. It is also:

Sensors attached to real equipment.

Networks carrying those signals.

Old control systems and patchy documentation.

Human teams balancing safety, maintenance, and output.

That physical layer changes everything.

A model can be excellent and still fail in practice because a sensor drifts, a camera is badly placed, a machine has been modified, or a maintenance team no longer trusts the alert stream.

This is where the safety stories connect to the economic ones.

If the data going in is weak, the decision coming out can be weak too. And if that decision touches physical systems, the cost is not just a wrong answer on a screen. It can be downtime, scrap, accidents, insurance claims, legal exposure, and lost trust inside an organisation.

None of that is well captured by a top‑level AI spending chart or a broad “AI exposure” metric. Yet it strongly shapes whether AI investment turns into real productivity gains or just more operational fragility.

4. Why that blind spot matters for AI and the economy

This is not a minor detail. It goes to the heart of how the AI boom is being interpreted.

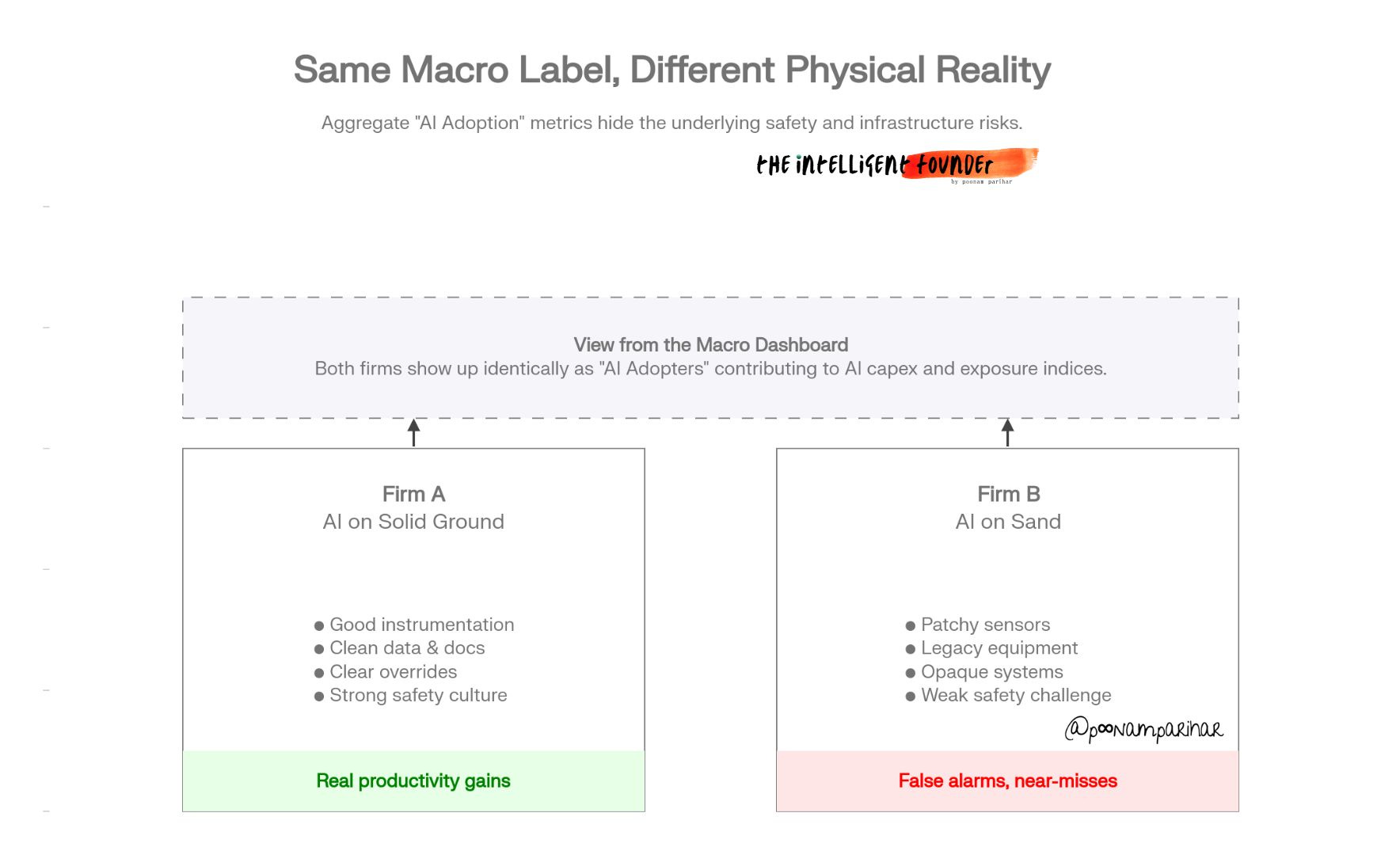

Two firms can both appear in the same macro story. Both are in AI‑exposed sectors. Both are investing in AI systems. Both are counted as part of the same productivity wave.

But on the ground, they may be very different.

One firm may have strong instrumentation, decent data quality, clear override procedures, and a safety culture that questions bad recommendations. Another may be running similar software on top of poor sensing, legacy assets, and weak operational visibility.

The first firm may see real gains.

The second may see false alarms, missed hazards, stalled rollouts, and a long list of “promising” pilots that never survive contact with the plant.