Borrowed Models, Owned Workflows: Thinking Machines's Story After Inkling

From DeepSeek‑lineage architectures to gigawatt NVIDIA deals, this is a founder’s read on whether packaging other people’s breakthroughs can become a durable AI business.

Thinking Machines has released Inkling, its first open-weights frontier model - a 975-billion-parameter multimodal Mixture-of-Experts system trained on roughly 45 trillion tokens, paired with fine-tuning tooling and day-zero support from ecosystem partners. Well Great, But I am slightly confused.

Last Dec I wrote an essay on Thinking Machines, on their for extraordinary $2 billion seed round at a $10–12 billion valuation for Tinker, a fine tuning API / training service, which wasn’t even released.

They actually din’t stop on that. there were rumors of a follow-on raise at $50–60 billion valuation.

Bloomberg reported in November 2025 that Thinking Machines was in early talks to raise a new round at around $50B, with some sources saying up to $55–60B.

Multiple follow‑ups ( such as Dealroom, Reddit, SiliconAngle, StartupHub) repeated the same story: post‑seed, they explored a follow‑on round targeting roughly $50–60B, which ultimately did not close.)

“My issue? – Tinker looked like a narrow wedge into enterprise AI.”

Tinker aimed at simplifying multi‑GPU fine‑tuning for LLMs, exposing low‑level primitives while hiding infra complexity.

Coverage framed it as an infrastructure tool for researchers/startups rather than a broad enterprise platform: a way to customize models, & not a full stack product with its own demand engine

This was when there was no commercial traction was visible so nothing really justified that valuation jump that was being floated.

Since then the company has added -

a gigawatt-scale NVIDIA compute partnership,

expanded Google Cloud infrastructure,

a genuinely novel real-time interaction architecture,

a January 2026 personnel exodus, and

now a frontier-scale open‑weights model, whose own launch materials admit it is “not the strongest overall model available today, open or closed.”

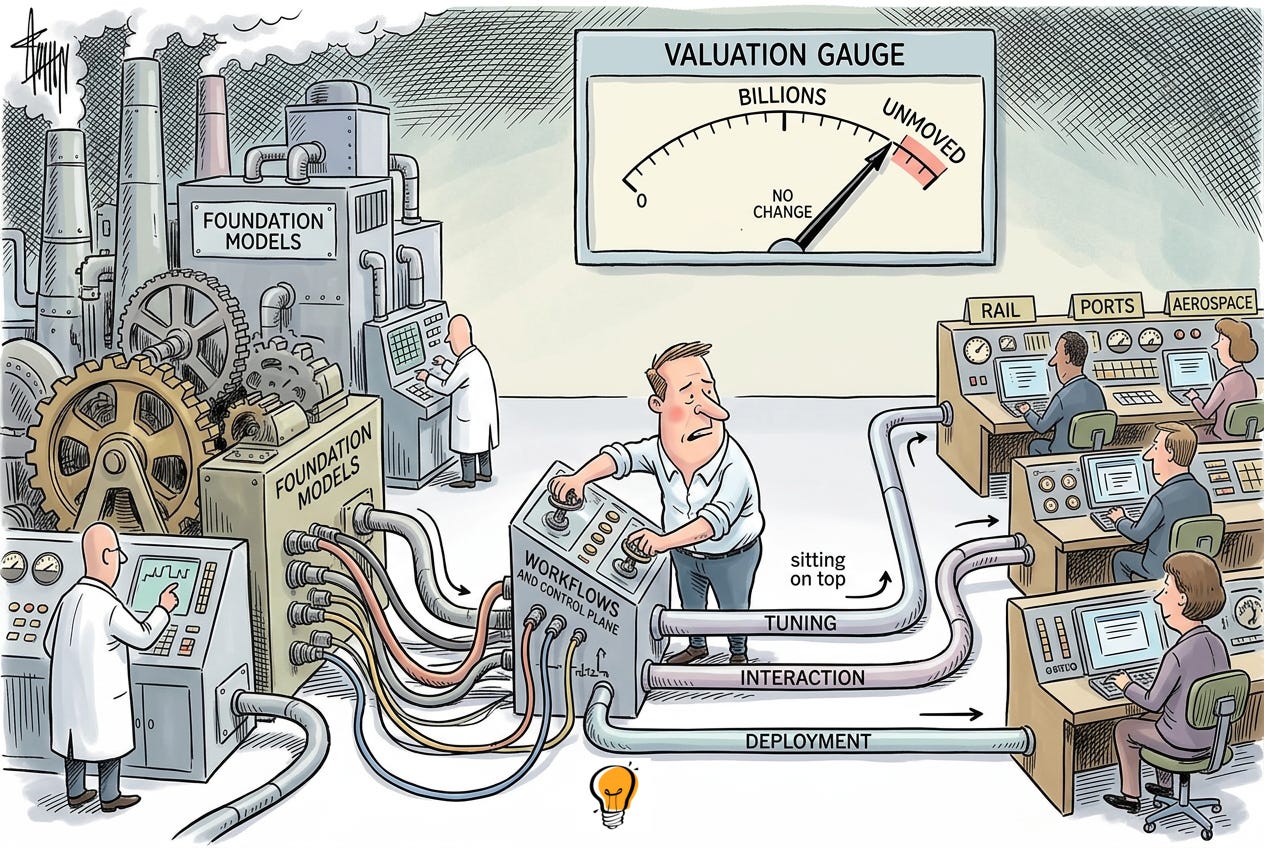

So from a AI lab, is Thinking machines now a story about whether a company can build a durable business by owning the control layer of AI?

- the tuning, interaction, and deployment layer that sits between raw foundation models and enterprise workflows - and btw using architecture largely borrowed from DeepSeek, without a single valuation number moving in a year of real shipping.

Table of content

Thinking Machines, Revisited: What I Got Right (And Missed)

The Six Months That Changed The Thesis

What Thinking Machines Says It Is

The DeepSeek Lineage: Borrowed Brains, New Wrapper

It’s All Branding, And That’s The Game

The Real Battle: Control Plane vs Chat App

Why They Didn’t Build Their Own Model

Valuation Reality Check

Can Packaging Be A Moat?

The Cleanest Way To Explain All Of This

Part 1: The December thesis, and why it was right but incomplete

For those who’ haven’t read the last deep -dive, Let me do a short recap on their past years or few months history. The starting point was pretty straightforward. Mira Murati, OpenAI’s former CTO, founded Thinking Machines Lab in February 2025. Within roughly five months the company closed a $2 billion seed round, the largest in the AI boom to that point, with reported post-money valuations ranging from $10 billion to $12 billion across different outlets. TechCrunch reported $10 billion, while Reuters and Wikipedia cite $12 billion. Andreessen Horowitz led the round, with NVIDIA, AMD, Cisco, ServiceNow, Accel, and Jane Street participating.

At that point the company had exactly one product:

Tinker, a cloud-based fine-tuning API positioned to make multi-GPU tuning feel like working on a single device, exposing a Python interface and hiding distributed orchestration from developers.

There was no publicly released foundation model, no clear revenue disclosure, and a mission statement about “human-centered” AI that read more like branding than strategy. My point? - investors were pricing a company aggressively on a single, narrow product with no visible traction data or just on a Famous Founder.

Worst part? The market was already reading Tinker as more than a standalone product; it was being read as a wedge into a bigger “control layer” strategy for enterprise AI, and later reporting only strengthened that interpretation. What I likely missing in my December essay was the sequencing » the fact that Tinker was never going to be the end state. It was the entry point into a much larger stack that would only reveal itself over now?. But I am still not fully sold on this thought process here, but I’d go with whats visible so far of their journey. I also don’t see lot of people doing a deep dive, except a Contrary Research’s in‑depth business breakdown, Sebastian Raschka and other practitioners writing technical notes on Inkling’s architecture and benchmark behavior comparing it with Deep Seek’s by why exactly? when its already known to be “inspired” from it?

Part 2: What happened in between - the timeline from Dec to Now.

Four major developments filled the gap between December and July, and each one deserves separate treatment because each changes what kind of company Thinking Machines actually is.

The NVIDIA deal, March 2026. Thinking Machines announced a multi-year, gigawatt-scale partnership committing to deploy at least one gigawatt of next-generation NVIDIA Vera Rubin systems, plus collaboration on training and serving architectures, alongside a significant additional NVIDIA investment on top of its earlier seed participation. On the surface this looked like standard NVIDIA playbook which is - invest, promise compute, strengthen hardware dependence and is exactly why it felt unremarkable at first glance. Strategically, though, it anchored Thinking Machines as a serious infrastructure-and-model company rather than an app/API startup, giving it the compute credibility needed to train and serve frontier-scale systems.

Google Cloud expansion, April 2026. The company expanded its use of Google Cloud’s AI hyper-computer, becoming one of the first customers for A4X Max instances built on NVIDIA Blackwell through Google’s infrastructure. This mattered less as a headline and more as confirmation that the compute story was not a one-partner dependency; Thinking Machines was diversifying its infrastructure base the way a company planning to operate at genuine scale would.

Interaction models, May 2026. This is the one genuinely original piece of technical work in the entire timeline. Thinking Machines published “Interaction Models: A Scalable Approach to Human-AI Collaboration,” introducing an architecture that processes multimodal input and output in roughly 200-millisecond micro-turns, breaking from the classic turn-based chat paradigm toward full-duplex conversation - a system that can listen while it talks. This part is NOT a DeepSeek clone or a borrowed pattern, it is actually a real research contribution, and it is the strongest evidence that Thinking Machines is building toward something beyond tooling and open weights.

Inkling, July 2026. and but finally, the model - 975 billion total parameters, roughly 41 billion active per token, a one-million-token context window, trained on approximately 45 trillion multimodal tokens, released with open weights and strong performance on audio benchmarks. TechCrunch called it the company’s “first public proof point after a year and a half building AI infrastructure largely out of public view.”

Sitting between these milestones was a fifth event worth naming precisely, because the loose version overstates it and the previous drafts underweighted it. In January 2026, several team members, reportedly including co-founder Luke Metz left and returned to OpenAI within the same week. Public reporting ties the departures to a disagreement over research direction and values, with one person leaving over an ethical disagreement and taking a handful of colleagues with him, rather than a mass exodus or evidence the underlying strategy had failed. This is a legitimate distinction -

the product roadmap did not stall. Interaction models, the NVIDIA and Google Cloud expansions, and Inkling all shipped on schedule during and after this period. So It was likely a personnel and culture story, not a strategic one, and it should be recorded honestly rather than folded into an indictment of the business model.

Put this all together, the story sequence now starts with

tuning,

layer in high-scale compute and deployment,

weather a personnel disagreement without missing a product beat,

publish a genuinely novel interaction architecture, and

finally ship a model whose weights you can actually own and adapt.

Part 3: But What Thinking Machines actually said it wanted to be

The company’s own mission language is useful here and not because “human-centered” or “human-will-extending” branding tells you anything about the underlying moat, but because it reveals the intended role in the AI stack once you strip the packaging away.

Thinking Machines says it wants to make AI systems more widely understood, customizable, and generally capable, and to build AI that extends human will and judgment rather than replacing it.

Translate this into product strategy, and this reads as three pillars.

First, train strong models - frontier-level multimodal systems like Inkling that reason across text, image, and audio and serve as a base for further adaptation.

Second, build tools for customization - Tinker and related APIs as the layer where enterprises and developers fine-tune, post-train, and shape model behavior to their own tasks, policies, and data. and

Third, develop richer interaction and deployment interfaces - the micro-turn, full-duplex architecture that lets humans and models collaborate in real time rather than through static one-shot prompts.

That combination is not “we have a model plus an API.” It is closer to a control plane for AI:

a place where organizations tune, monitor, and interact with models in ways that encode their own values, operational constraints, and workflows.

The underlying bet is that the bottleneck in AI adoption is shifting from raw capability to fit. -

fit to domain,

fit to policy,

fit to human judgment.

and if I am right here, the most valuable layer in the stack is not necessarily the largest model but the system that makes models adjustable and deployable in the real world.

Part 4: The DeepSeek lineage - is borrowing the architecture a the strategy, not a failure of it

Honestly, I am skeptical on this one. This is the detail that reframes everything else, and it deserves to be stated plainly rather than softened.

The Information reports, and Thinking Machines itself has confirmed in briefings, that Inkling’s architecture “largely follows” DeepSeek V3 - the Chinese Mixture-of-Experts model that proved a design built on Multi-Head Latent Attention, auxiliary-loss-free load balancing, and multi-token prediction could close the gap with closed frontier labs at a fraction of the training cost.

Deep Seek v4 was making much news earlier in March. the whole drama about release timing, geopolitics, and pricing pressure rather than just raw benchmark which btw made lot of folks in West nervous. It’s become a kind of Rorschach test for open‑weights, China’s AI ambitions, and the sustainability of the current model‑provider business.

so now when Inkling has arrived, which is an example of what you can build on top of a good-enough V3‑lineage base. DeepSeek V4 has already sucked most of the oxygen out of the room:

a noisy preview cycle, hand‑wringing in Washington and Brussels about “AI dumping,” and a model that mattered less for its evals than for what it signaled about China’s ability to ship cheap, near‑frontier open‑weights at scale. But still Lets give it some time -

Inkling’s parameter profile mirrors V3 lineage almost exactly in shape:

975 billion total parameters versus DeepSeek’s 671 billion, 41 billion active per token versus DeepSeek’s 37 billion - the same family, scaled up. TechCrunch further reports that some of Inkling’s early post-training data came from Moonshot AI’s Kimi K2.5 before reinforcement learning pipelines took over.

None of this is hidden.

It is, in fact, the strategy working as designed.

Thinking Machines has never claimed it wants to win the architecture-invention race. Its own launch materials admit Inkling “is not the strongest overall model available today, open or closed” - an unusual admission for a frontier lab, and one that only makes sense if the business does not depend on topping leaderboards.

Wired’s coverage adds a stranger footnote from training:

the model at one point spontaneously decided that writing out its reasoning in natural language was inefficient overhead and stopped doing it, forcing researchers to reinstate legible chain-of-thought so outputs stayed explainable - a reminder that even borrowed architectures produce genuinely unpredictable behavior at scale, and that the post-training and safety work required to ship them is real engineering, even if the base design is not novel.

Spending years trying to out-architect DeepSeek would have delayed the thing that actually matters to this business model?

for example, getting a credible open base into developers’ hands quickly, then monetizing the tuning, evaluation, and infrastructure layered on top of it.

DeepSeek did the hard, path-breaking architectural work.

Moonshot is pushing the same open lineage further with Kimi K3, which now trades blows with Claude and GPT on coding leaderboards.

Thinking Machines is not trying to compete at that layer. It took a proven architecture, scaled it, trained and post-trained it at significant engineering cost, and wrapped the result in tooling, infrastructure, and an interaction layer that is, notably, its own invention.

That is not frontier invention at the model layer.

It is coherent, deliberate assembly at the platform layer - and the distinction matters enormously for how the business should be judged.

Part 5: This is all branding - and that is the point!

A fair objection raised throughout this deep dive is that “human-centered,” “trustworthy,” and “open” tags, all of which are largely PR wrappers, and the pattern is visible across the entire industry, not just at Thinking Machines, so they are just following the herd.

Anthropic markets trustworthiness while repeatedly navigating security controversies.

OpenAI marketed “open” while becoming one of the most closed labs in the industry and absorbing assets like OpenClaw into a tightly controlled ecosystem.

The useful move is to separate messaging from mechanics entirely: “human-centered” means “we want the product framed as augmenting people,” but tells you nothing about the actual moat.

“Trustworthy” is shorthand for safety positioning or compliance posture. “Open” in AI has become especially slippery.

it can mean open-source, open weights, open research, or just a vaguely more accessible product, and those are very different commercial commitments.

The real questions that cut through the branding are structural:

who controls the weights,

who controls fine-tuning,

who controls deployment,

who controls the data flywheel, and

who captures the enterprise relationship.

That is why “open” companies can still be very closed in practice, and “safe” companies can still be aggressively competitive. the branding exists to reduce friction with users, talent, regulators, and investors, while the business model does the actual work underneath it.

For Thinking Machines specifically, the interesting part is not the slogan but the structure:

first a customization wedge (Tinker), then infrastructure alignment (NVIDIA, Google Cloud), then a model release that expands the platform story (Inkling), with “human-centered” and “open weights” functioning as positioning language for the same underlying scramble for control that every major AI company is running. Different labels, same fight for control of the stack.

Anthropic enters through safety, OpenAI through breadth and convenience, Thinking Machines through controllability and leverage, but all are trying to own the same critical layers: model ownership, customization, deployment, distribution, and enterprise lock-in.

Part 6: The competitive map - control plane, not chat app

I was wondering if Tinker was ever a flagship product or would Inkling be. and I’ll explain why. It din’t have a fancy launch. and a limited release to few research orgs. Now Compare this with Anthropic and Open AI, the fellow AI labs. Claude and ChatGPT solved a fundamentally different problem than the one Thinking Machines is solving. They became things people ask for by name - habits, defaults, verbs. Thinking Machines shows no visible effort to build anything like that:

no breakthrough consumer interface, no canonical developer surface people reach for first, no obvious “this is the product” moment beyond an API and a model release.

Compared against xAI, the contrast is instructive.