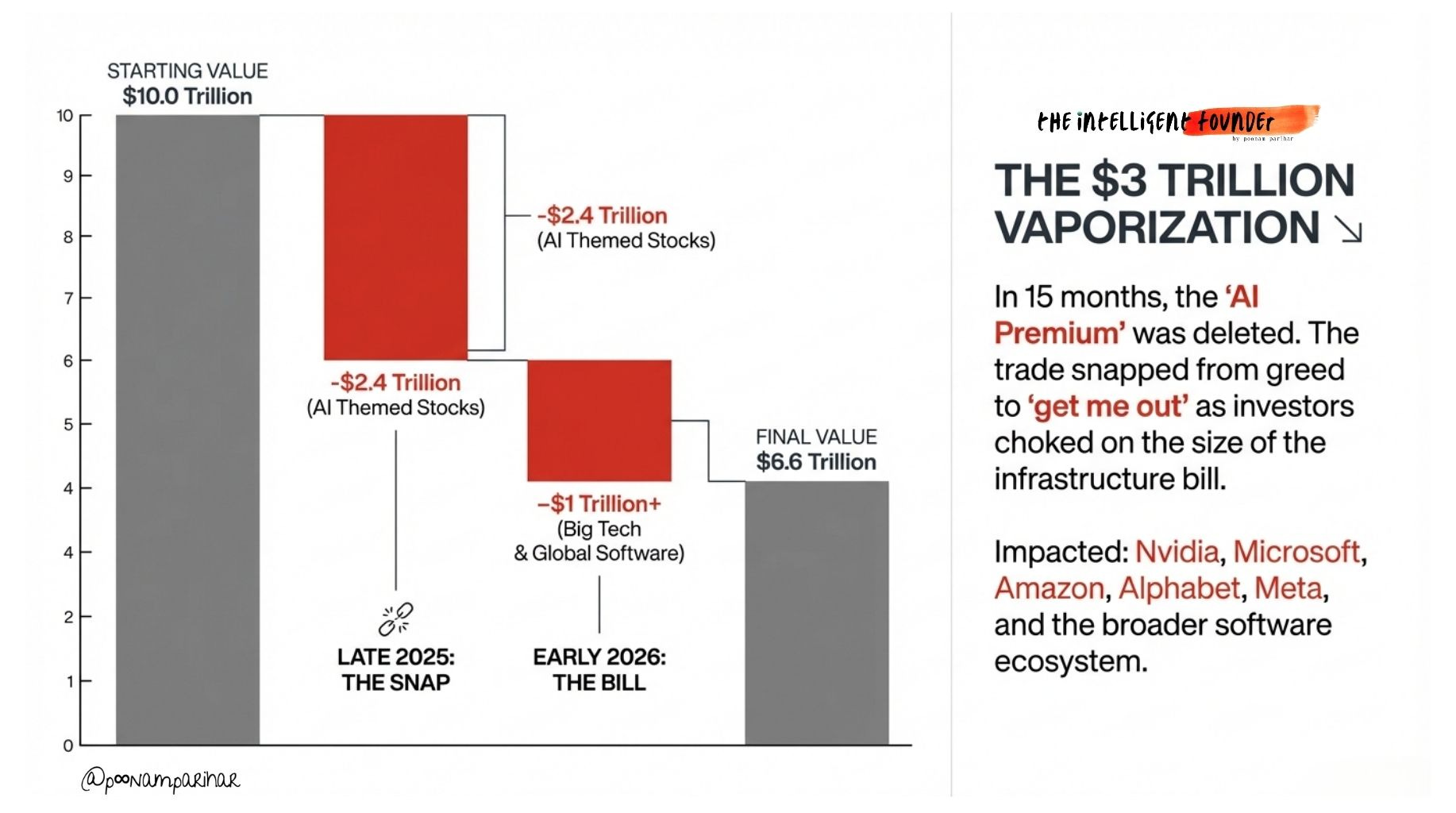

Over the past 15 months, AI‑linked stocks have done a full round‑trip from euphoria to humiliation, twice.

In late 2025, nearly 70 “AI winners” in the U.S. shed around 1.8 to 2.4 trillion dollars in value as the trade snapped from greed to “get me out.” In early 2026, Big Tech, software and services names gave up another trillion‑plus as investors finally choked on the size of the AI infrastructure bill.

The shockwaves were global.

Indian IT and services majors saw about 2 lakh crore rupees wiped out in a day, with the Nifty IT index down 6–7% as markets suddenly priced in the idea that AI agents might do app dev, testing and maintenance more cheaply than offshore armies. London‑listed software and data businesses were pulled into the same downdraft, and European analytics names were hammered on “AI eats SaaS” headlines.

Claude Cowork Headlining the crash story.

Into that nervous setup, Anthropic dropped Claude Cowork. Overnight, investors had a vivid demo of an AI “co‑worker” that can draft code, review contracts, respond to customers and crunch data across tools.

Claude Cowork did not cause the February crash on its own, but it gave the rout a villain and made the threat to software seats and billable hours feel suddenly concrete. It landed exactly when people were already asking whether hundreds of billions of AI capex would ever show up in earnings, and it turned a fuzzy fear into something you could picture on a P&L.

Jefferies analysts even branded the reaction a “SaaSpocalypse,” arguing that the narrative flipped from “AI helps SaaS and IT” to “AI replaces SaaS and IT” almost overnight.

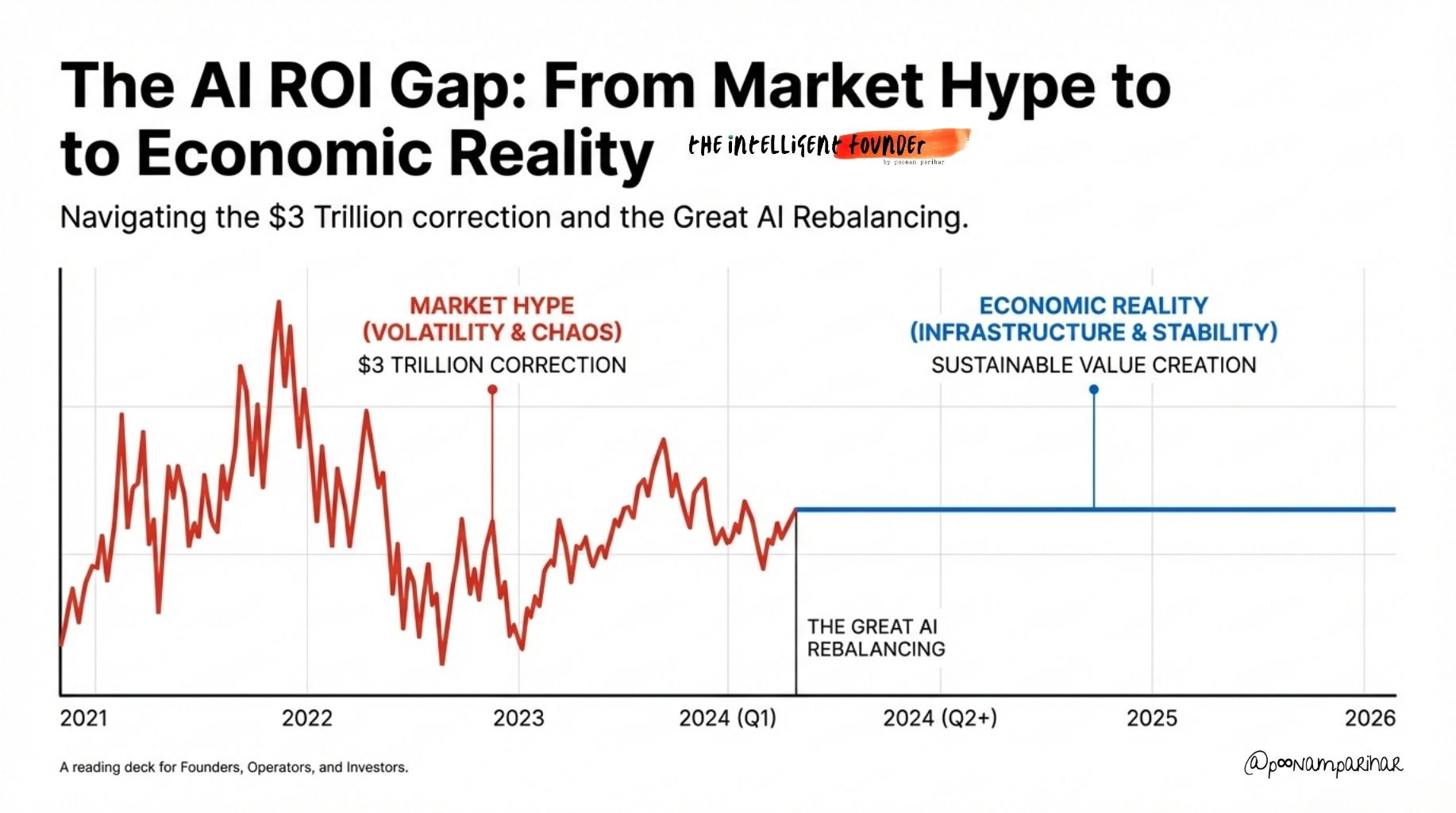

The AI ROI GAP

On the surface » this looks like “the AI bubble bursting.”

Under the surface » the behavior of the people actually signing the cheques says the opposite.

Hyperscalers are still marching AI capex higher, not lower, and are openly committing hundreds of billions of dollars to data centres, GPUs and custom silicon. If they thought AI was a fad, they wouldn’t be betting their future margins on it. Analysts and strategists now talk openly about AI compute demand as a multi‑year secular trend, not a 2023–24 fad.

The Great AI rebalancing

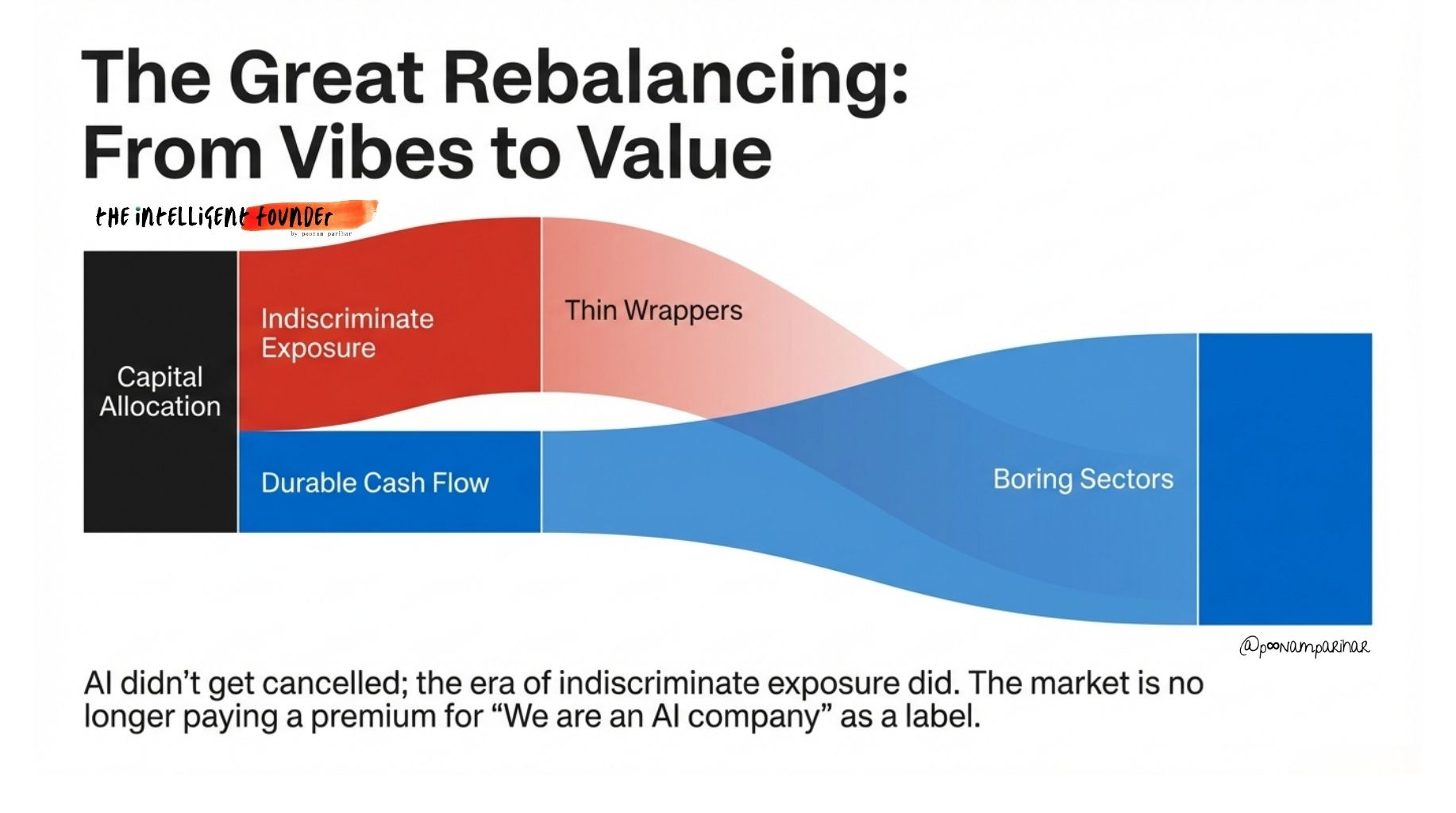

Underneath the headlines, we’re in what some analysts call the “Great AI rebalancing”: the market is rotating out of “buy anything with AI in the deck” and into “show me durable cash flow plus a sane valuation.” The concentration in a handful of mega‑cap AI names is easing, and capital is flowing back into boring, cash‑generative sectors that quietly use AI rather than sell it.

In other words, AI didn’t get cancelled; the era of indiscriminate AI exposure did.

What has burst is not belief in AI. It’s patience for lazy AI economics.

Investors no longer pay a premium for “we’re an AI company” as a label.

They are asking boring, brutal questions:

what happens to your gross margin when you include inference costs,

how fast does AI spend turn into cash, and

what stops someone else with the same model eating your lunch?

A lot of this comes down to what some market notes now call the “ROI gap”: the uncomfortable distance between the billions going into AI chips and data centres, and the much smaller, slower stream of AI‑specific revenue and margin showing up in earnings.

As long as that gap stays wide, boards and funds will keep asking the same question:

which products actually close it, and

which are just riding the narrative?

Indian IT and global consulting are being repriced around the idea that any role defined by repeatable digital work is now vulnerable to automation. SaaS names whose “moat” is a thin wrapper around public models are getting marked down accordingly.

For Employees, default career ladder is changing

For employees especially juniors and offshore developers, this shows up as a very personal story: articles literally titled “Fear factor: Claude Cowork, techies no work?” are signaling that the default career ladder is changing.

For CIOs and CTOs, it’s a cold shower.

They’re still told “you need an AI strategy or you’ll die,” but they’re now punished if AI projects don’t come with hard numbers and fast payback.

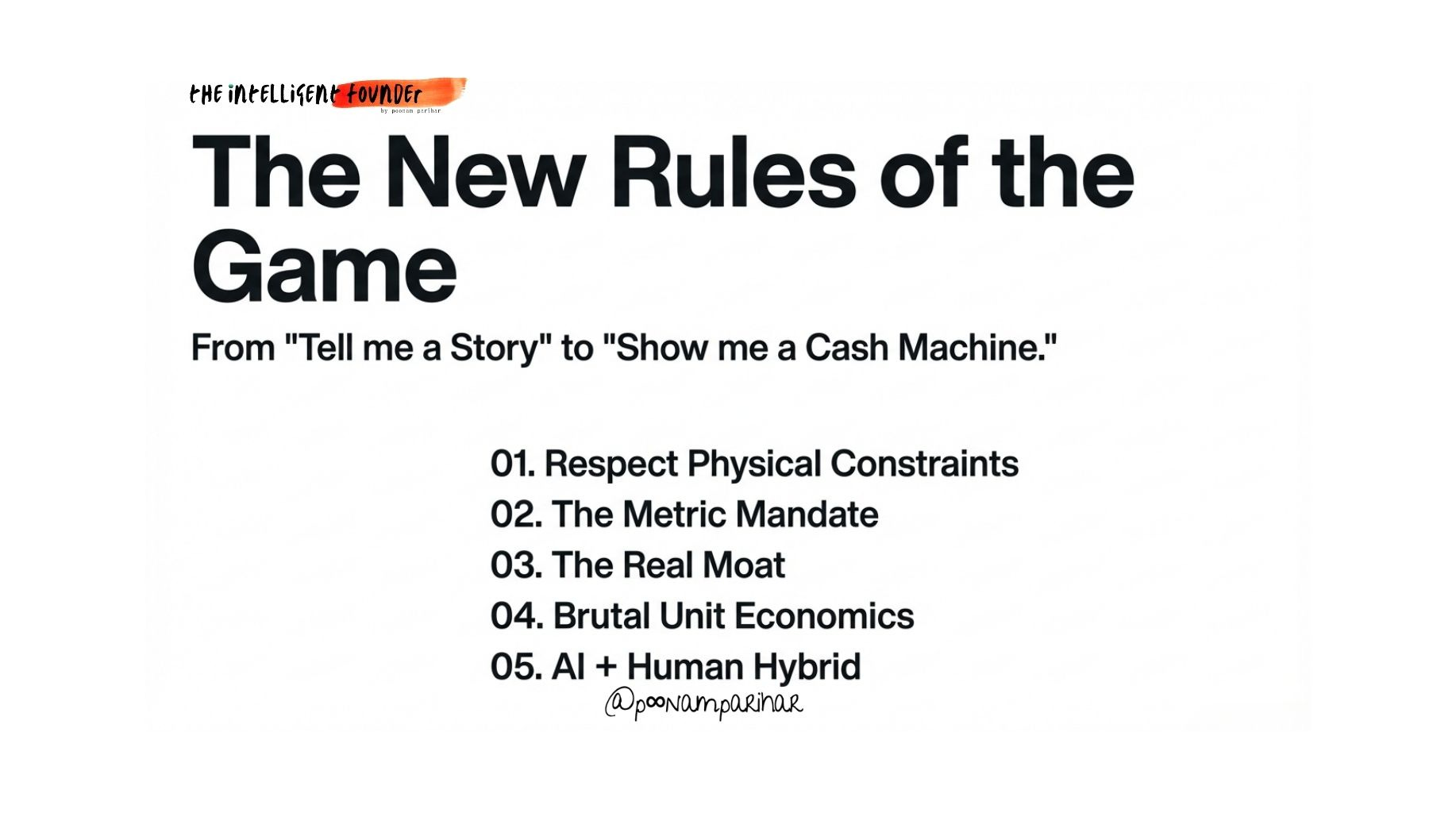

For founders and operators, this moment is uncomfortable, but incredibly clarifying. The market has quietly rewritten the rules from “tell me a big AI story” to “show me an AI cash machine.”

If you assume from day one that infrastructure is expensive, investors are sceptical, and customers are allergic to vague productivity claims, you’ll design a very different company.

Practically, that means a few things.

1

first, you plan your business as if AI compute stays pricey and limited, so capacity isn’t “just a cloud setting” but a scarce resource » you budget, test and manage like any other.

2

Second, you force every AI feature to hook into a metric an operator cares about » hours saved, deals closed, risk reduced, and you instrument it so the before‑and‑after shows up in a dashboard, not just a deck.

3

Third, you treat access to models as table stakes, not a moat; the defensible layer is your proprietary data, your integration into critical workflows, and your distribution, not the fact that you call the same API as everyone else.

4

and Fourth, you learn to talk about AI unit economics in language a non‑technical investor can understand and you design for AI plus humans, not AI instead of humans—AI takes the grunt work while humans bring judgment, trust and edge‑case handling.

The good news is,

that this phase rewards builders who already think in unit economics, workflows and customer value.

The bad news—for some—is that it punishes anyone still optimizing for vibes. If you’re already in the “AI must earn its infra bill” camp, this isn’t your crisis; it’s your filter.

In other words: the routs are not a verdict that “AI was fake.” They are a very expensive filter.

What’s getting flushed is flimsy AI storytelling and thin wrappers.

What’s left on the other side will be products and companies that can look an infra bill, a skeptical investor and a battle‑hardened operator in the eye and still make sense.

If you can build that kind of business while everyone is doom‑scrolling AI crashes, you’re not on the wrong side of history, you’re building the boring, compounding layer that the next hype cycle will quietly depend on.

In this episode we covers

💥 3T of “AI premium” just got wiped, and that’s healthy for real builders.

🏗️ Hyperscalers keep pouring hundreds of billions into AI, signaling real demand.

👩💻 Claude Cowork became the global “AI might eat my job” scare moment.

⚖️ Capital is rotating from vibes and thin wrappers to real, provable value.

📘 Playbook: price in costly infra, prove ROI, build real moats, and use AI to upgrade humans.

If you enjoyed this episode and want more deep‑dive playbooks like this, consider subscribing and if you’re getting real value for your work or company, becoming a paid supporter helps me keep doing it.